Policy Pitch: Cap the CAP

How to get off the path of property tax ruin

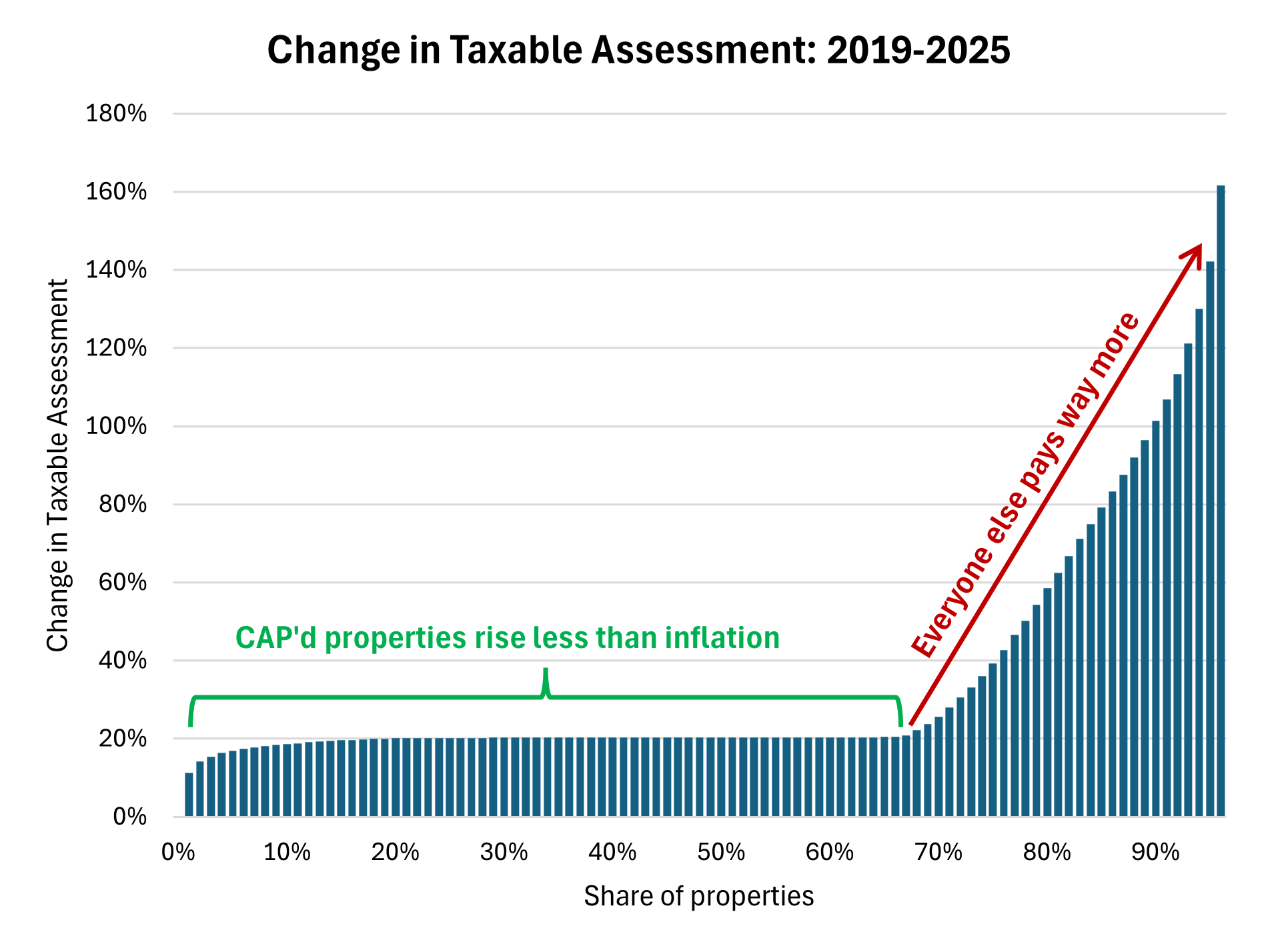

Halifax councilor Janet Steele initiated a motion for staff to study the Capped Assessment Program (CAP). The CAP is a provincial program which limits assessments value increases to the rate of inflation for owners of 1-4 unit properties.

The CAP has many problems. But an important one for Halifax’s council is it completely obfuscates councils tremendous austerity. For example, last year council kept the tax rate flat, so for CAP’d properties (roughly 85% of properties), their tax bill rose by just 1.5%. And yet everywhere in the media — articles touted a 4.7% in the average tax bill. “Average” in this context is meaningless, combining the vast swath of CAP’d properties, uncapped large apartments, and the dreaded resets that happens when properties are sold (which can result in a near doubling of the tax bill). For one, staff must start reporting the median change in tax bill, which means exactly what the typical person thinks of as “average” or “typical” and would be more appropriate since the median will always equal the CAP rate, apply to the large majority of residents.

That quibble aside, it’s quite something to see councilors try to reconcile the notion that their constituents feel to be at their breakpoint with affordability and terrified of losing the CAP, with the reality that those owners may be paying half the taxes of their new neighbors. The truth is we’re under no obligation to be reasonable when it comes to our opinions about taxes. But it is our elected representatives jobs to be responsible with their tax policies. There’s nothing responsible about our current system, where huge tax bills are put on young families so established owners need not pay for their profits.

But how do you reform this? The last reform effort faltered in 2019, and the CAP was a much smaller factor before the COVID housing boom.

While council clearly is responding to the growing chorus of upset movers and young families paying much higher tax bills, seniors still dominate the voter base municipally. And they can look at their true market valuation of their home and shudder: simply removing the CAP would cause many properties to be assessed at rates up to double. That’s not fair to do — because council would cut the rate — but it is what confused seniors do. Heck, some of our elected leaders have based entire platforms on confusing seniors about the difference between tax rates and tax bills. It is fertile soil.

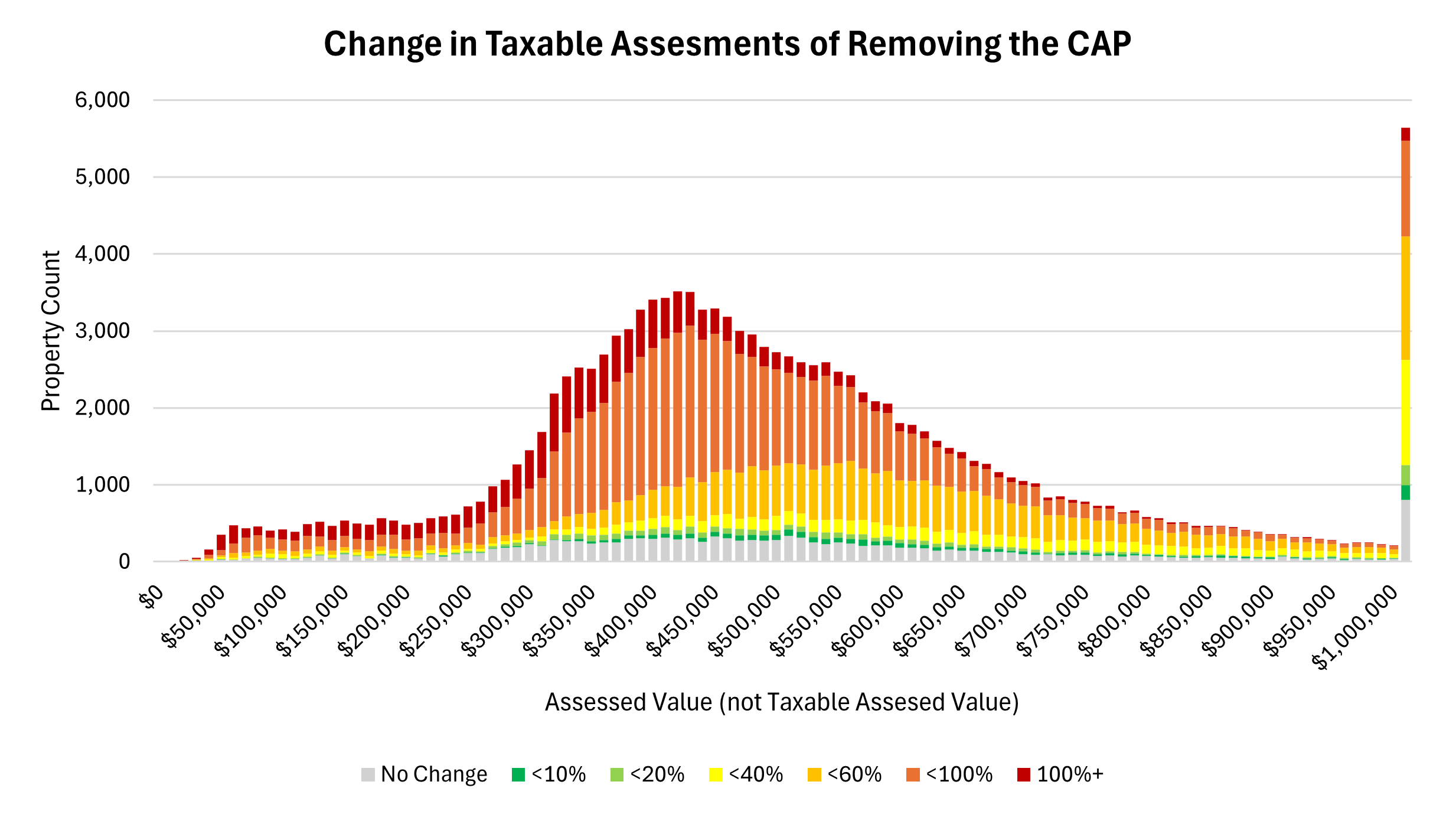

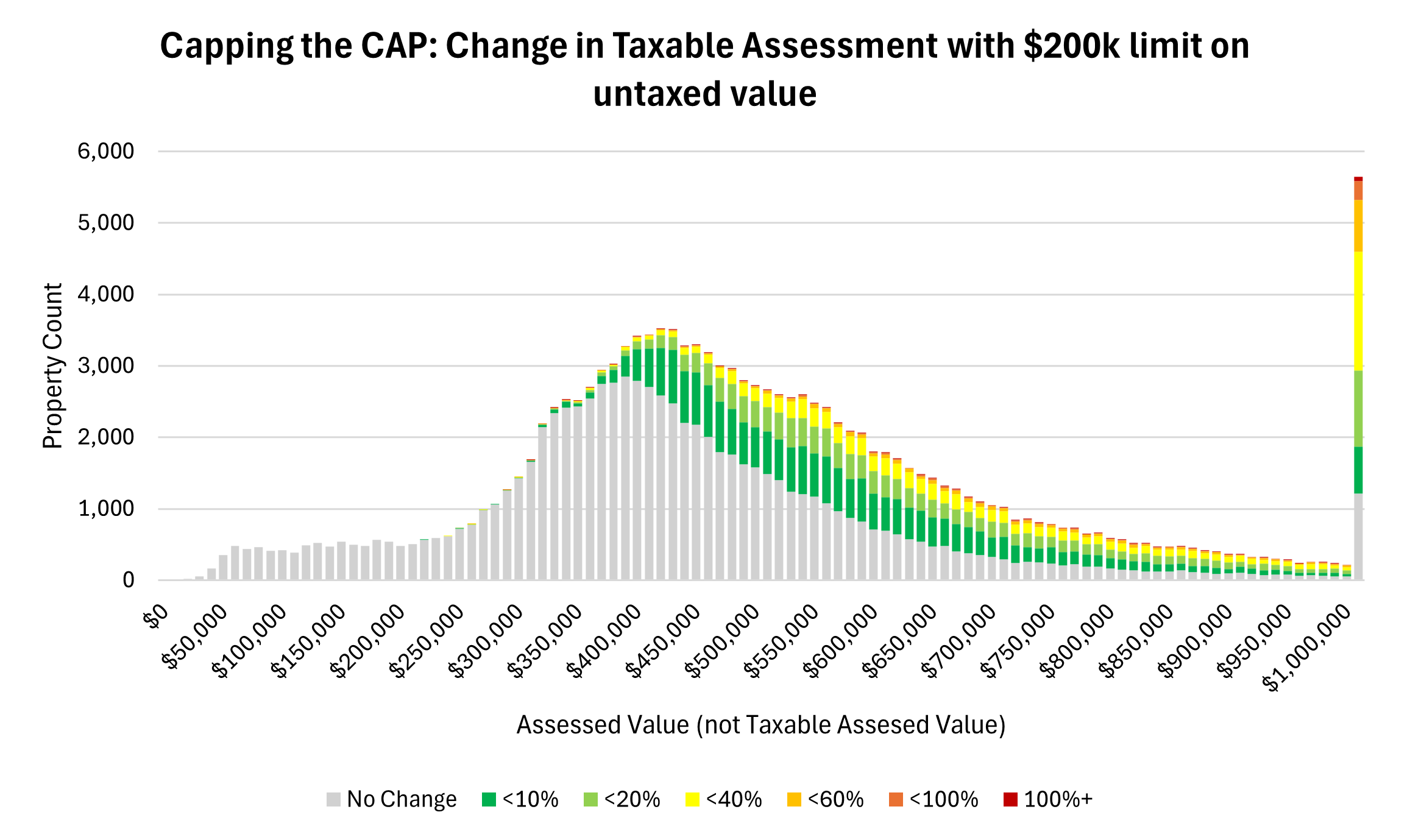

Obviously — eliminating the CAP is out of the picture. We hardly talk of the CAP at all, especially provincially. But I’ll put my cards on the (reform) table. I would cap the CAP: limit the amount that Assessed Values can diverge from Taxable Assessed Value to a fixed dollar value. Lets set that at $200k.

So, if you own a $400k home taxed as a $200k home, you see no change. But if you have a $800k home taxed at $400k, you’d start getting taxed at $600k. Illustrative examples aside, we can show how this would affect taxable assessments with data.

What I like about this approach is it allows you to make sweeping claims, Like no one with home value below $400k will be affected. Or that 80% of properties will see less than a 10% increase. Meanwhile, you’ll really cut down on the horror of having mansions not being taxed on over $3.4 million dollars of home value.

This change effectively targets high valued properties, who have large gaps between their CAP’d value and the market value, and by definition have made money on their homes. But the reform doesn’t aim to raise revenue per se. In fact, in this scenario it only cuts the amount of untaxed home value by 15% (equivalent to some $27 million in municipal revenue). Instead it offers an off-ramp to this insane system of landed tax gentry. It allows the CAP to slowly fade away, as homes reach their $200k limit, instead of accelerate year by year. Paired with a clause to let first time homebuyers keep CAP’d assessments, Cap the CAP and Keep the CAP are the outlines of a measured but substantial set of reforms to get us off this path to tax hell.

Kudos to councilor Steele for initiating the discussion.

Has the staff report Janet Steele requested been presented to Council?

Why not allow for deferrals that would be paid out at sale of the property? So a cap while the current owner remains in place (perhaps adjusted per your value gap proposal), with the unpaid portion to be recovered when the owner sells?

I believe that other jurisdictions have similar deferral programs, often targeted to seniors, though that comes with its own challenges. Could means test if needed.

The CAP sounds a lot like Prop 13. Is it inheritable if an owner leaves the property to a child upon their death?