Policy Pitch: Keep the CAP

Protecting First Time Homebuyers from Punishing Tax Increases

Nova Scotia’s Capped Assessment Program (CAP) limits how much assessments for the purposes of municipal and provincial property taxes can increase. CAP-eligible properties have assessment increases limited to inflation, as measured by the Nova Scotia Consumer Price Index (CPI). Any 1-4 unit properties owned by a resident (including investment properties) are eligible, meaning that most property owners are covered by the CAP.

In the past 5 years, the rapid run-up in home price has driven a significant wedge between assessed home values (benchmarked by home sales) and taxable assessments (limited by the CAP). That wedge can be comforting for homeowners fearful of property tax increases.

However, the CAP does not last forever, and taxable assessments reset to market assessments upon sale. Increasingly, homebuyers are seeing their property tax bills explode past the prior owners and their neighbors, due only to this provision of the CAP program (the reset).

For example, the median eligible property in HRM (where detailed data is available) is assessed at $475,000. However, it is only taxed at $299,000. A new buyer for that property will see their tax bill rise by about $150 per month in the year after the purchase. It is not clear that homebuyers, realtors, or even financial institutions are aware of these pending large tax increases.

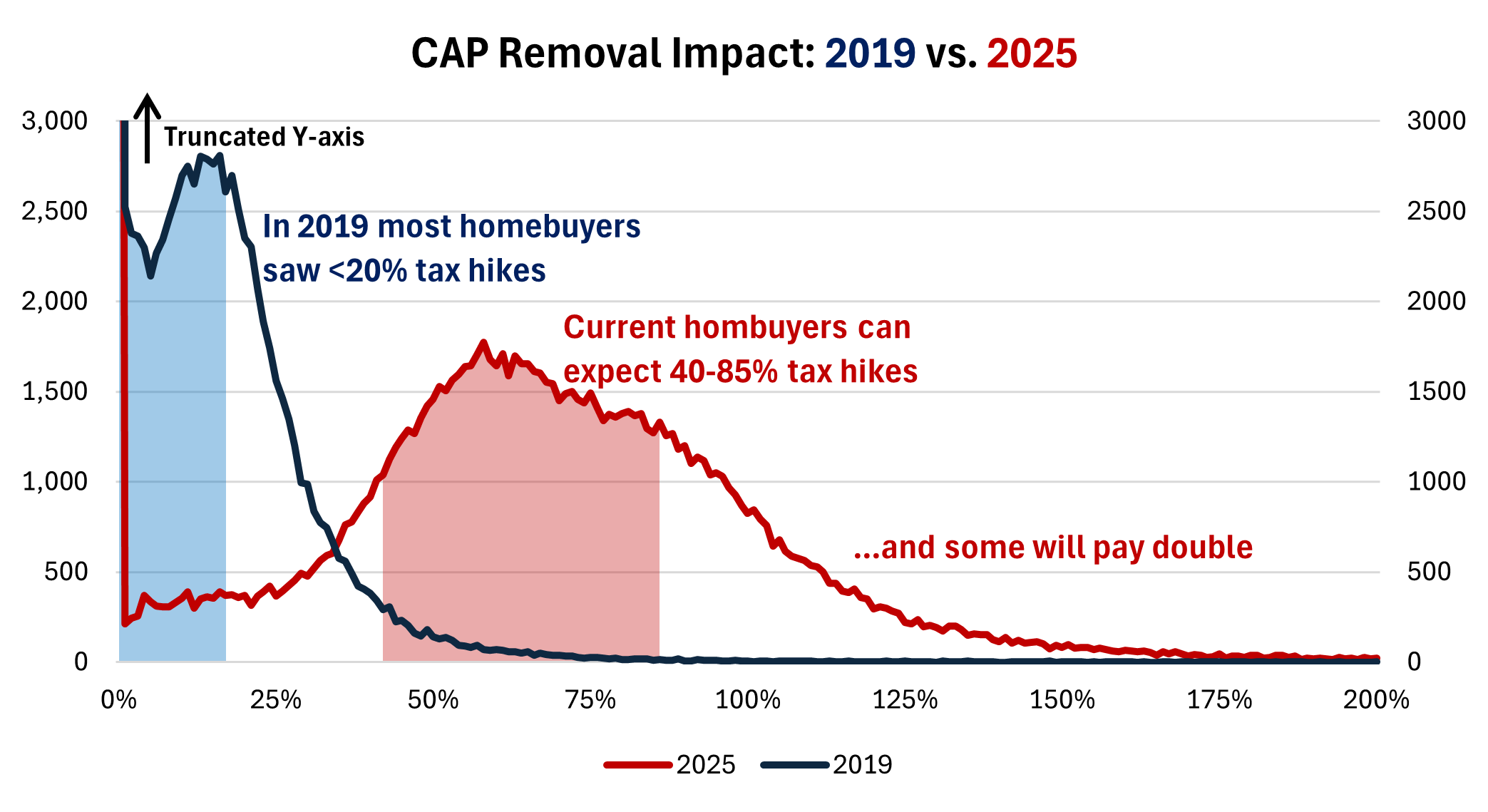

While the CAP is an old policy, dating back to 2005, its problem are accelerating. Five years ago, the CAP could be ignored for most properties. 40% of properties saw no CAP removal impact, and only a fifth would increase assessed values by 20% or more. Now, only roughly 1 in ten properties can ignore the cap, and buyers can expect a 45-85% increase in their assessment. About 15% of properties will see their tax bill double or more.

First-time home buyers are already struggling: prices have risen, interest rates remain high, and the cost of rent continues to hamper savings. Far from enabling homeownership, the CAP targets home buyers, including first time home buyers, with punishing tax increases.

There is a simple fix. The provincial government should change the CAP to not reset when a first-time homebuyer purchases a property. This practice already exists, for within-family sales, and was also invoked for reconstruction of the properties destroyed by the 2023 wildfires (reconstruction also triggers a CAP reset).

This change would help first time homebuyers when they are already struggling to make ends meet. The change would also tilt the playing field — favouring first time buyers over investors and speculators, who would still face the higher tax bills if they bought these “family homes”.

It could also be done at minimal fiscal cost. Municipal revenues are determined partly by assessments, but also by tax rates. The only impact would be that assessments would rise slower than otherwise.

For example, (conservatively) using assessment figures for HRM, this change would slow the assessment roll increases by $875 million per year (assuming roughly 5,000 FTHBs per year). Nova Scotia’s assessment roll tallies up to $147 billion currently, meaning this change would reduce the increase by 0.6% per year.

If the policy change needs a “pay-for” CAP eligibility could be removed for properties valued over a $1 million. This would apply to roughly 4% of properties and raise assessments to offset two years of first-time homebuyer CAP freezes. Additionally, limits or removals of eligibility for investment properties, which have profited greatly from the housing crisis could also offset the change (detailed data not available).

In the end, having homeowners with identical properties pay vastly different tax bills is a bad idea - especially when it targets young families. I wonder how long we continue to do this to 2-3% of the population, year after year.