Nova Scotia's property tax problem grows

On leverage, the power of compounding and bad policy design

I’ve written before about Nova Scotia’s unique property assessment cap program. The other day, the PVSC released its updated assessments for the 2024 calendar year. As a reminder, the PSVC uses sales data for their assessment, but with a two year lag, so the 2024 assessments are based on 2022 home sales.

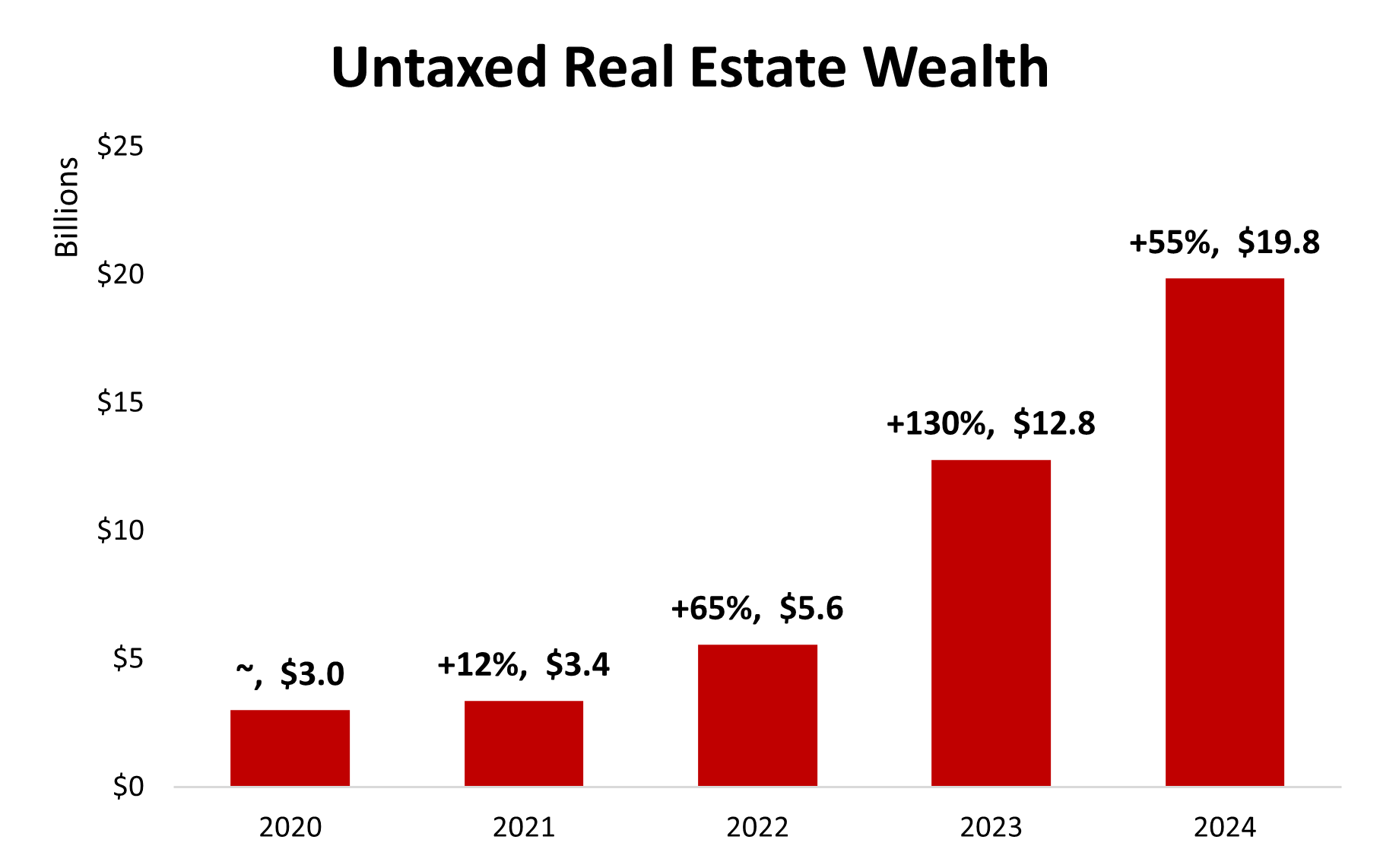

2022 was a big year for house price gains in Halifax, so the assessment data came in strong, up 16% over the previous year, to $96bn. But more importantly, the taxable assessment value (which includes CAP protection) increased by 9%, to $77bn. At this point, over 20% of the assessed value of HRM properties is not being taxed.

Pop quiz!

Question : If Assessments increased 16%, and taxable assessments are up 9%, how much did the wedge (untaxed housing wealth) grow?

It’s not 7%. It’s 55%.

That massive difference is because the levels of each measure are different, so the growth in the gap is amplified. In my line of work, businesses with mostly-fixed costs and growing revenues call that operating leverage. A railroad that grows revenues by 5% and keeps cost flat adds 12% to their bottom-line.

That’s a great dynamic for railroad investors, but in this context means CAP protected real estate value should be expected to rise quickly. Over the next decade, if assessments rise 4% per year, and taxable assessments rise 2%, the untaxed value would rise 8% per year, up to $50bn by 2034. Under those numbers, only 65% of HRM’s assessed value would be taxable.

There are many more factors at play1 , but the point is that, under the status quo, we should expect CAP to become more important over time.

Revenue-Neutral Reform

I’ve caught some flack on twitter about describing the gap between assessments and taxable assessments as untaxed wealth. That’s because municipalities like HRM also manage tax rates to get a desired revenue. Meaning, the you can argue that CAP only changes the relative tax burden across property owners. The logical solution is to eliminate the CAP, and deliver a big cut in property tax rates to get the same revenue. That would cut taxes for everyone who doesn’t have a low CAP’d value, including some who may *think* they are winning with CAP (e.g, a rate cut of 20% would overwhelm an assessment increase of 15%)2.

I think that’s a fair approach, but not the only one. The biggest drawback is that some folks with a $150,000 home will see big tax increases. I think that’s one reason that nothing has happened, despite the NS Federation of Municipalities lobbying against CAP.

Easing off the CAP train

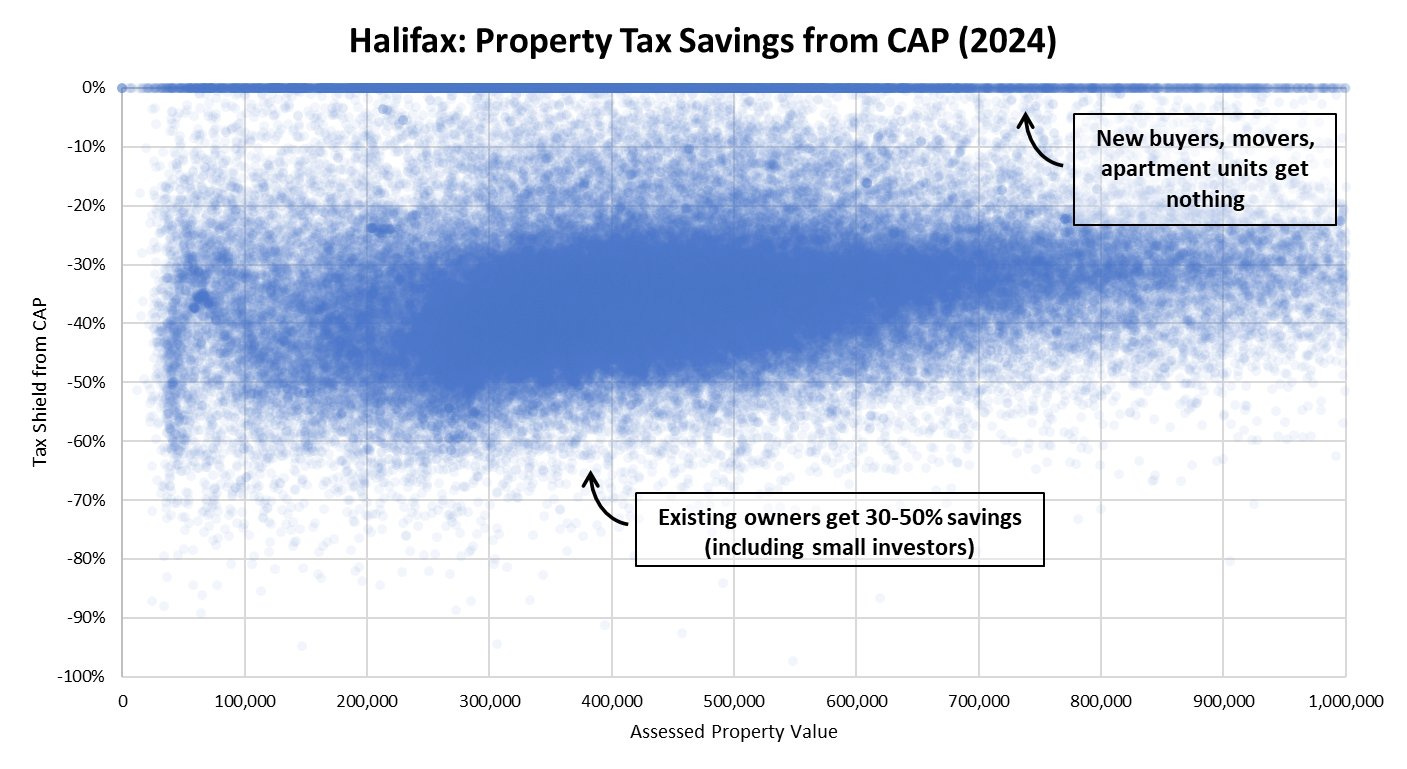

My suggestion would be to cap the CAP. Set a maximum dollar amount that your Taxable Assessment can be below your Assessment. Let’s say that’s $150,000. That means a $300,000 home being taxed as a $150,000 home would not see an assessment increase, but a $1,000,000 home being taxed as a $500,000 home would see their assessment increase to $850,000. What’s critical here is that percentage-wise, expensive homes get just about as much CAP benefit as small homes currently (see the first scatter chart).

This change would allow policy makers to clearly tell homeowners below something like ~$350k (actual math pending..) that they will not see an assessment increase. And that most of the extra taxable assessment value would come from rich homeowners!

Some rough calculations suggest this reform would cut the untaxed value by 20%. It can be dialed however you like (setting the limit to $100k cuts untaxed value by ~40%). That extra money could be used for anything, including cutting rates.

That might seem like a big effort to only shave off 20%, but don’t forget: house prices go up. Over time, more and more homeowners would hit that $150,000 limit and their taxable assessments would start to rise in-line with actual assessments. It would get us off our current track where CAP becomes a larger and larger force in our decisions about where we live and how our cities raise revenue. It is undoing the bad leverage dynamics and replacing them with positive leverage dynamics.

Other benefits of my approach vs. the revenue neutral approach:

No tax cuts for big apartment owners

No tax cuts for out of province owners

Essentially creates a progressive property tax among the ~60-70% of homeowners with CAP

Finally, when you are dealing with such a bad policy, nearly any change will be an improvement, but we need to do something, or we risk watching this problem grow even more.

That’s all for now, though I might get back to the assessment roll and what it means for HRM’s budget.

E.g., House sales reset CAP values, new homes get added, etc.

A CAP researcher has estimated the breakeven at ~27% for 2024. If your CAP’d assessment less than 27% of your actual assessment, you’d be a winner after the big rate cut.