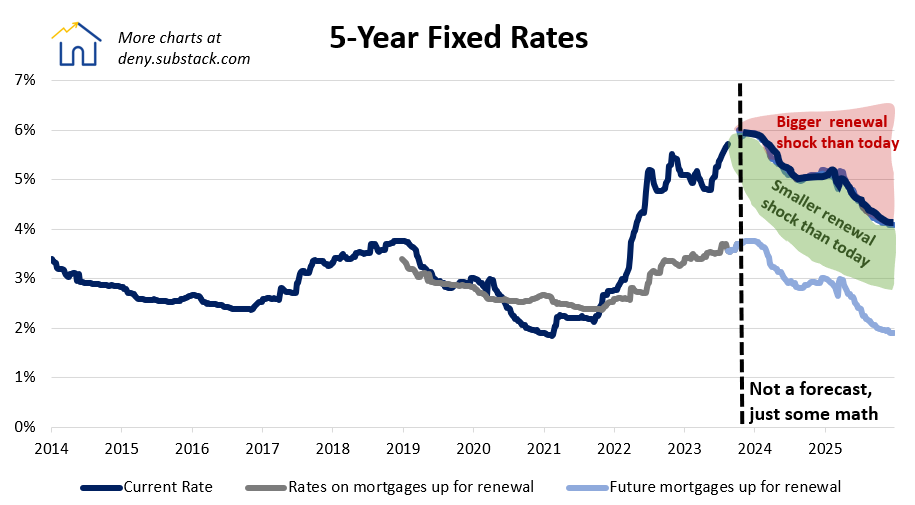

Interest rates need to fall a lot to avoid mortgage renewal pain

Pandemic-era mortgages with lower rates are getting closer to renewal

It’s clear that we are living through a high-interest rate moment1. For Canada’s highly-indebted households, higher interest rates are a concern, especially as our mortgages - unlike the U.S. - do not have fixed interest rates for 30 years.

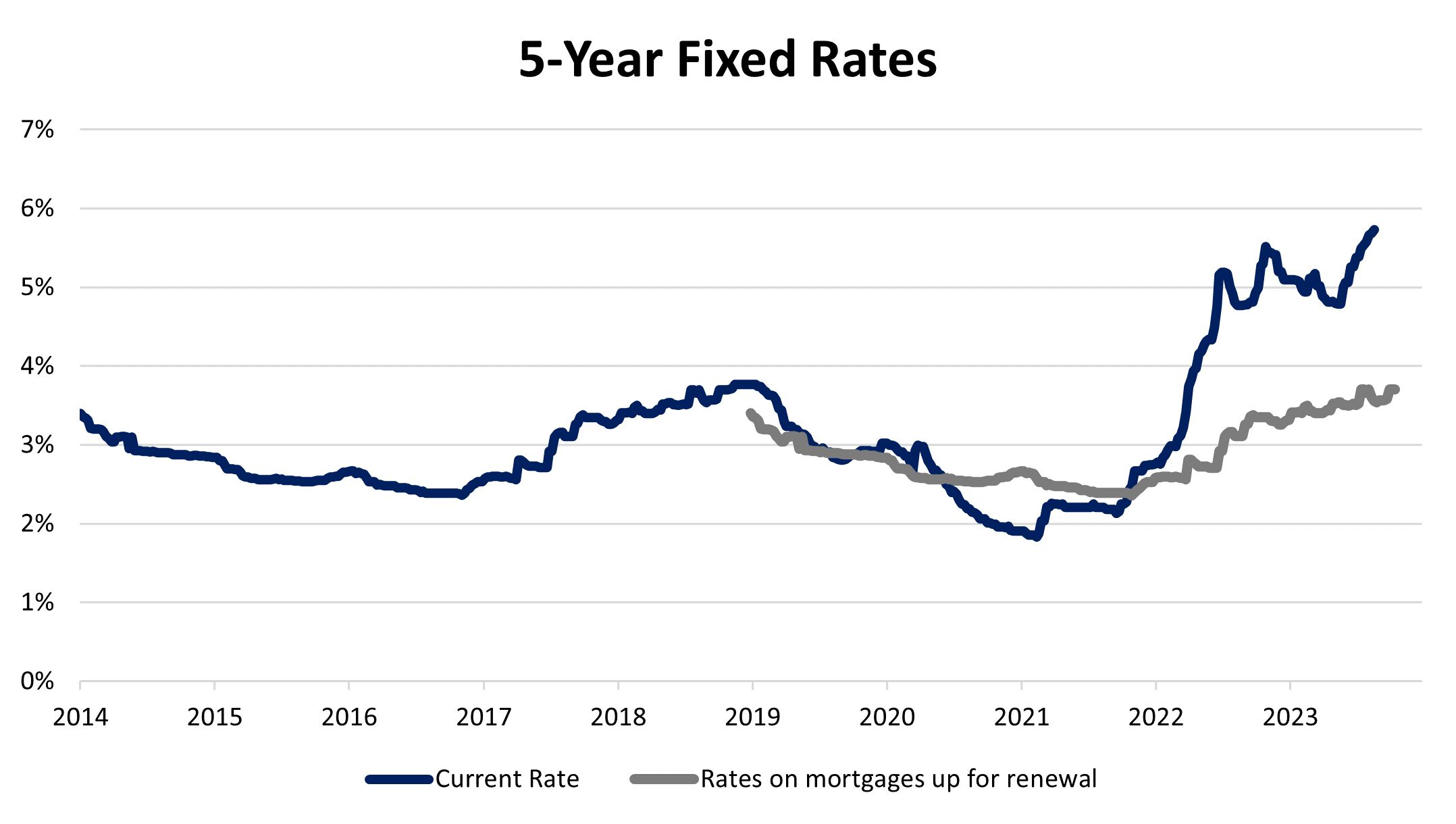

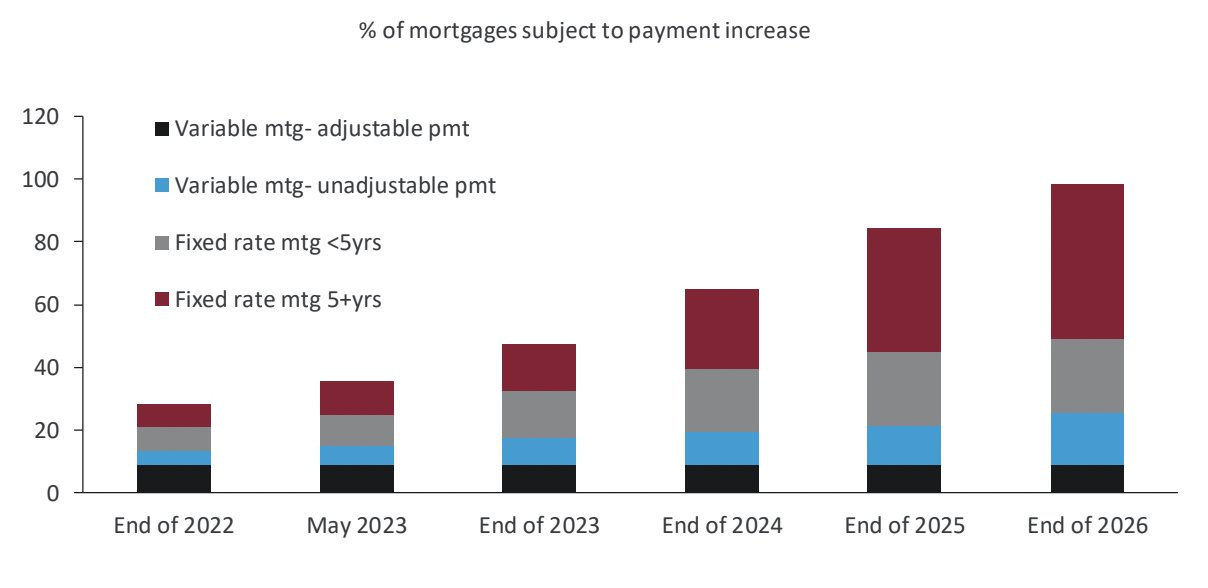

In Canada, the most important mortgage is a 5-year fixed rate. That is also the longest fixed rate period available from most banks. Even though new lending has shifted strongly away from “locking-in” recently, about ~40% of bank mortgages are 5-year fixed rate mortgages2.

I’m going to focus on the 5-year fixed rate. As of late August, the average 5-yr fixed rate was 5.7%, and it’s probably around 6% by October3 . That’s big problem for new buyers - but it’s also a problem for homeowners, because, 5 years ago that same mortgage rate was ~4%. So homebuyers from 2018 who chose a 5-year fixed would now be renewing their 4% rate into a 6% rate. On a $400,000 mortgage, that rate increase can add $500 a month in interest.

That will be tough for many household budgets to handle. But what worries me is that 2018 was a modest high point for mortgage rates. And for the next few years, the mortgages that are coming up for renewal will have lower and lower (original) interest rates.

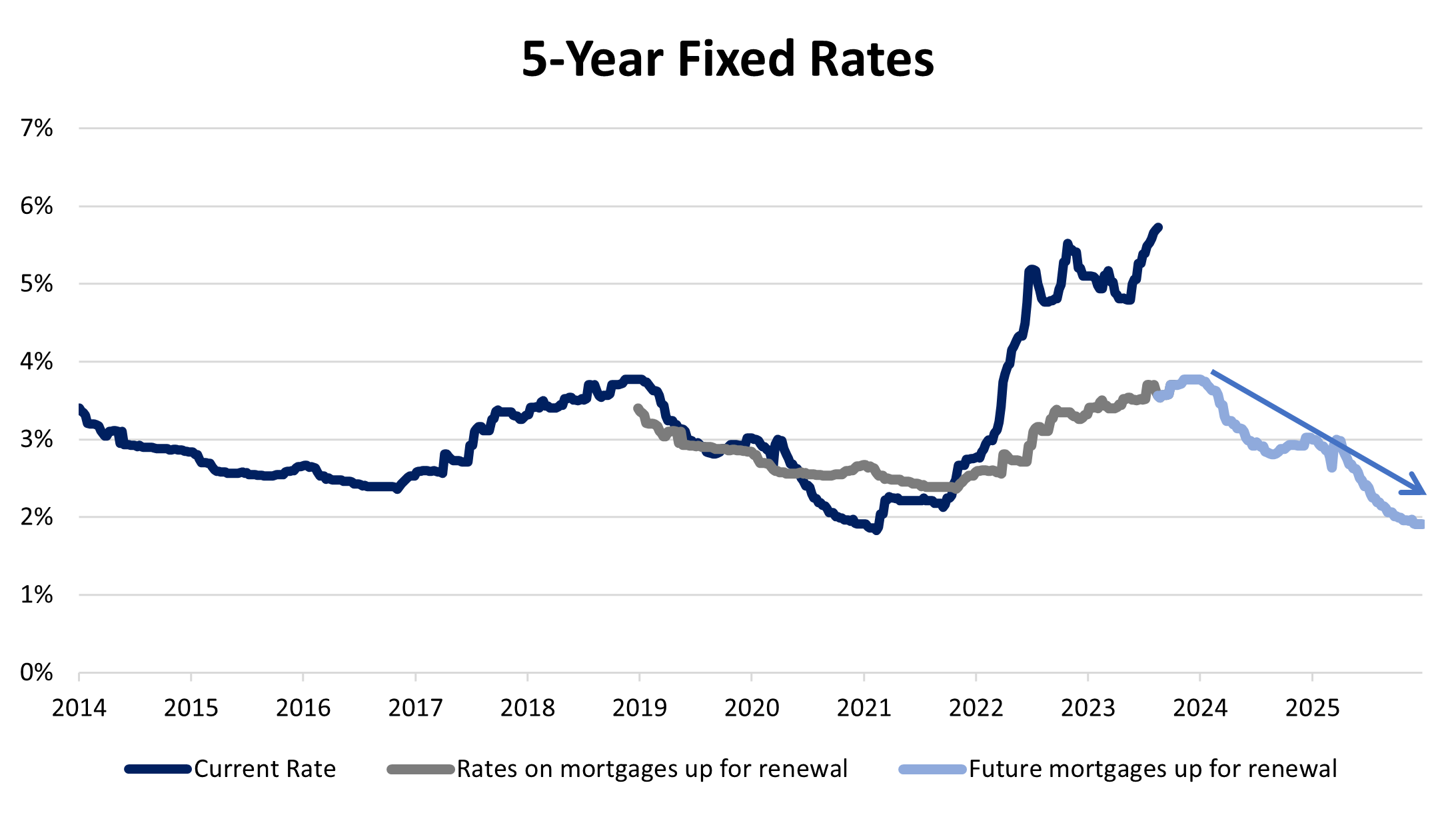

Nobody knows where bond yields (and thus mortgage rates) are headed. But we know with great accuracy what the mortgages up for renewal will be. While the mortgages up for renewal today average about ~4%, by mid-2024 those mortgages up for renewal will have a rate of ~3%, and by mid-2025 those rates will be about ~2%.

That means, compared to today’s tough renewal situation, it’s not enough for mortgage rates to fall - they need to fall a lot to avoid renewal payment increases getting worse.

Basically - if 5-year fixed rates fell to 5% by next summer, renewing borrowers would still face a 2 percentage point rate increase. If rates return to 4% by late 2025, borrowers would still face a 2 percentage point rate increase.

It should also be noted that the mortgage balances will be larger. By 2021, the average new mortgage was 25% larger than in 2018. And, as CIBC research shows, there are many such mortgages coming up for renewal in 2024 and 2025.

Homeowners have options. Re-amortizations are one. Short-term interest rates can move quickly, which could allow folks to switch away from 5-yr rates. And all these buyers have been stress tested at at minimum of a 5.25% interest rate.

Based on the experience of variable rate mortgage holders (from banks who’s payments adjust with the Bank of Canada rate - like Scotia), we should not expect a wave of defaults & forced selling. But, it is still concerning for the economy. Our GDP has already stalled on a per-person basis, and having many homeowners forced to devote hundreds of dollars a month more to mortgages means less money for shopping, restaurants, and the big-ticket purchases like cars that really drive the ups and downs of the economy. And widespread job losses could throw a wrench in anyone’s ability to pay off a mortgage.

The bottom line is that interest rate impacts from 5-year renewals have been relatively smaller so far due to higher starting rates. Meanwhile, for the next two years, mortgages up for renewal will have successively lower starting rates, which could deliver a lot of renewal pain for Canadian households, and squeeze the spending needed for the economy to grow.

That can be debated depending on your frame of reference (pre-2007 vs. 2010-2021)

The rest being a mix of 1-2-3-4 year fixed and variable-rate mortgage products

Fixed rate mortgage rates are closely tied to Government of Canada bond yield + a premium, so you can check how bond yields have moved to get a real-time sense of where fixed rates are headed

Deny,

Some nice graphs to make your point that we need to see rate drop to save home owners from falling off a cliff into the ocean.........Who cares?

Your on your own homeowner and don't wait for the banks or the feds to save you.