Higher housing costs are inevitable

Aggregate housing costs will rise despite where prices move

One of the most important features of the housing market is that very few people buy homes in any given year, and many already own a home, or several. It’s a big purchase, so it’d be wild for everyone to buy and sell homes every year. But it introduces lots of “lag” to the market. House prices may be high today, but most bought their homes long ago, when prices were much lower.

That opens the door to a stock-flow perspective of how much the average owner might pay. There’s a proper way to do this1, but I’m gonna cut a lot of corners and do the “fun with numbers” version here.

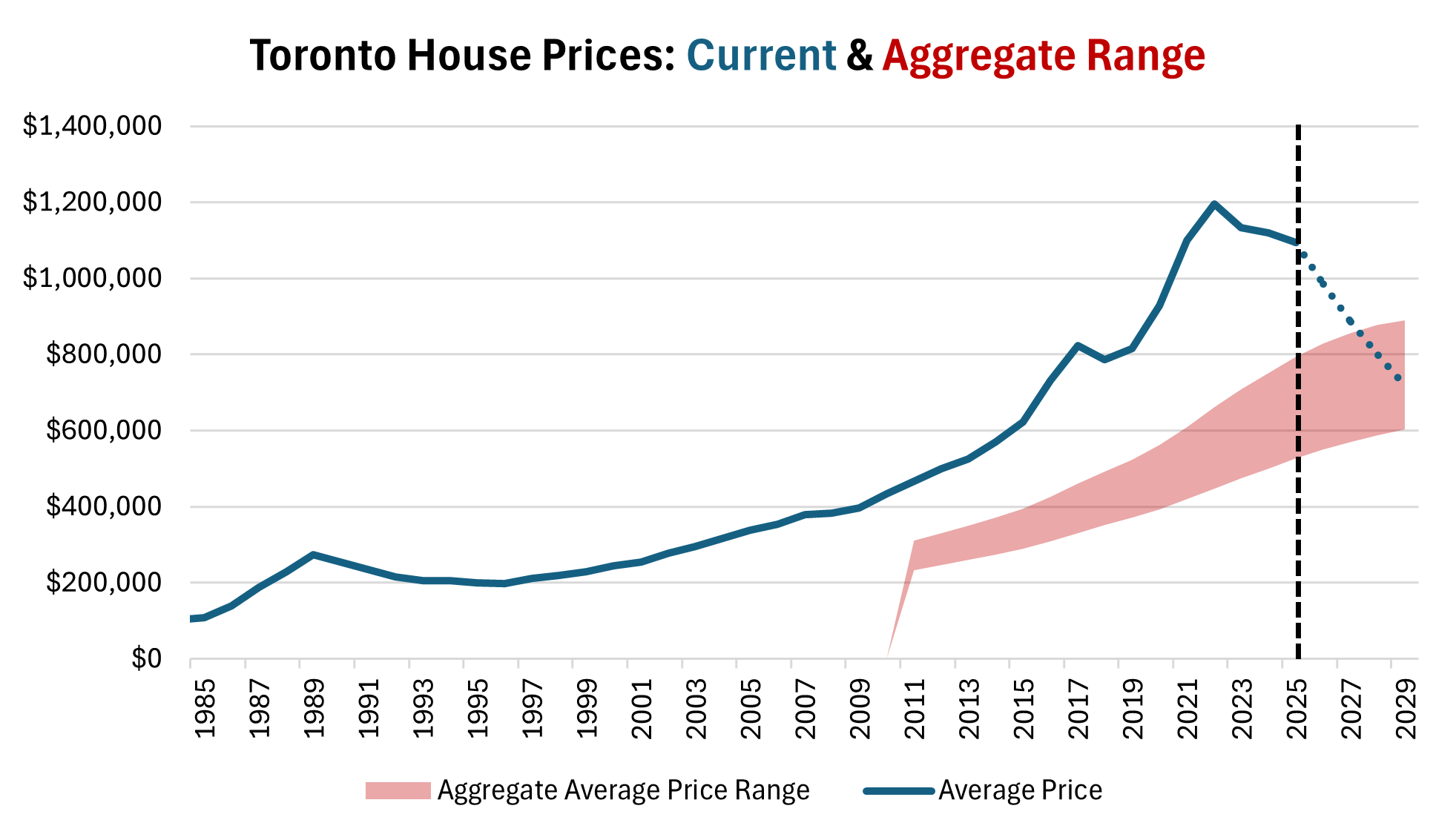

Toronto’s regional real estate board (TREB) has a long time series of home sales. Home sales bounce around quite a bit, but have averaged about 90,000 per year over the past twenty years. As of the last census, the Toronto region had 1.4 million owner-occupied homes (and another 700k renter households). That means that a typical year sees about 6% of the owner occupied housing stock sell.

Ignoring the distribution of homeowner tenancy, that means the aggregate housing bill will be something like the 20 year average of past home sales. It’s likely lower, as many homes will be sold within a few years (folks moving up the property ladder), and other homeowner have owned their home for 30 years or more.

So, while house prices in Toronto currently average about $1.1 million, the average amount paid - including past sales - by Toronto homeowners is likely far lower, between $800k2 and $500k3.

The aggregate range should always be lower than current market prices, but the point is to see how it can evolve under different scenarios for current prices.

If you assumed the worst case (or the best if you are a future buyer) of 10% price declines for the next 4 years, the average house price would fall to $715k (a 40% decline from the 2022 peak). But, because of the lag, the average aggregate would continue to rise, and just barely plateau.

The point is, regardless of where prices go for the next few years, the housing market needs to continue to find buyers able to afford far larger mortgages than past generations. And that even large price declines might not lower the financial burden of the housing crisis, even as it crushes enormous paper wealth among homeowners.

You’d want to link home sales with how long since the last sale, and would likely want to adjust for rented condos, among other things I haven’t considered

fixed 6% turnover scenario

half turnover scenario to account for re-sold properties

House prices depend on buyers’ income. Prices go up when residents’ income increases. This takes account of wage inflation over time which feeds directly into prices for homes. Lower wages or higher taxes will lower prices, but will make no difference to affordability. Complaining about house prices will do nothing for anyone. Houses are always expensive when you are buying and too cheap when selling.