Pension funds can be housing champions

Pension funds can be housing champions

The right investors, the right need for capital

Recently, a group of business executives penned a letter asking Canada’s finance ministers to “encourage” Canadian pension funds to invest more at home.

University of Calgary professor Trevor Tombe (my old macro prof!) explained why this would be a bad idea. I mostly agree with his take. But there is a space where pension funds could find (and fund) a win-win trade. Unsurprisingly, I think that’s housing. But first, a bit about pension investing.

The Urgent need for Patient Capital

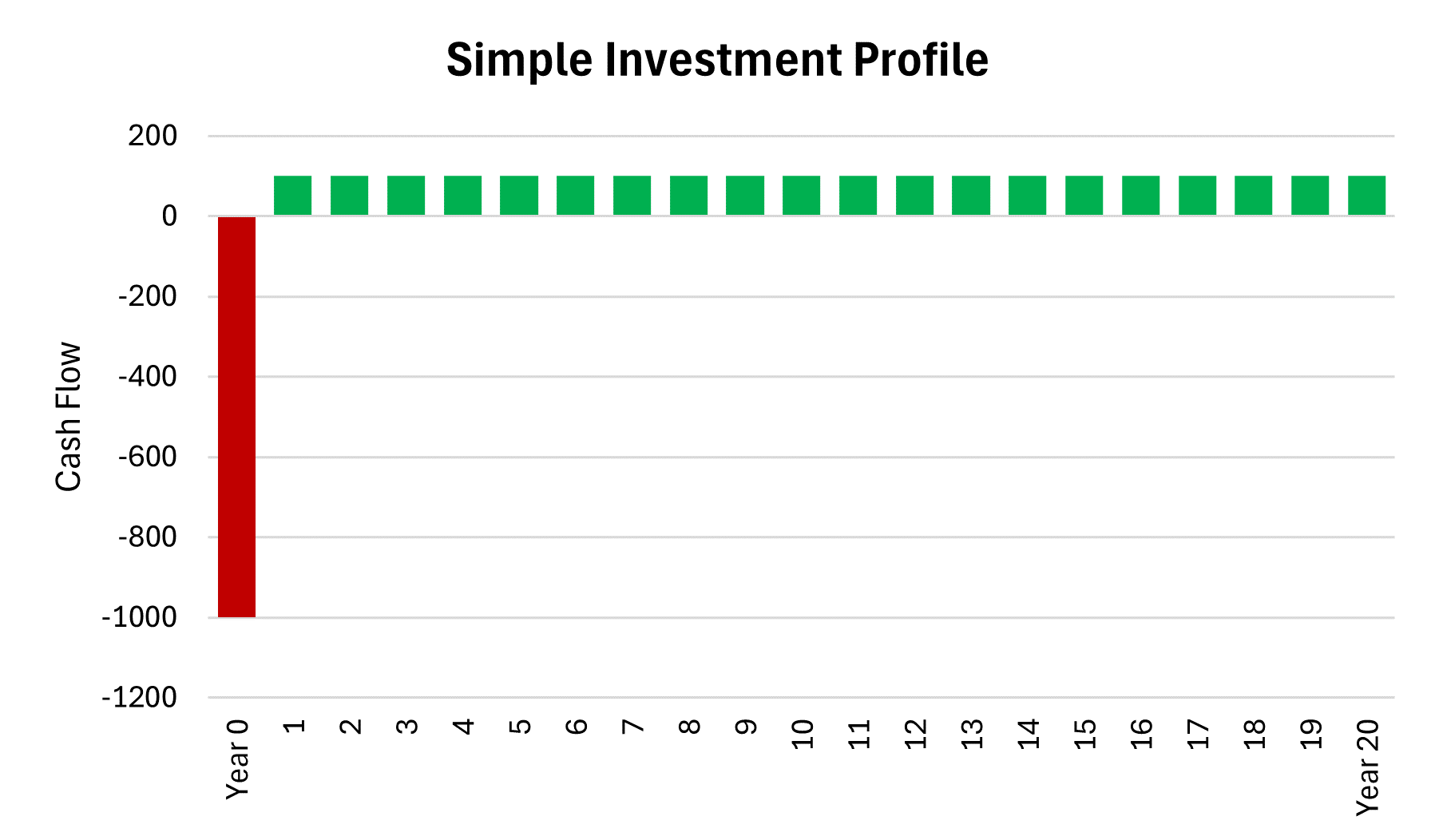

Pension funds are highly unique investors. They collect contributions from workers today, and will pay distributions years or decades later. Because we all age one year at a time, this process of collecting and paying out money is an unusually predictable process. This predictability and long-term focus makes it possible for them to invest (some of) their money with pay-back horizons that are very long.

That, along with lower bond yields, has spurred pension funds to invest more into real estate and infrastructure. These investments often involve cutting a big check today in exchange for lots of future smaller checks (or a far off big check).

Many investors (and especially their clients) would struggle to wait 5+ years to start earning a profit on their investment, but that’s exactly what pension funds specialize in.

Notably, this is the defining problem of real estate investing. It takes a ton of upfront money to build an apartment1. Rental income may be 3-5 years away from the start of construction2. But once built, buildings last decades3.

Dude, where’s my (investment) vehicle?

Clearly, it’s not like the pension funds are unaware that they could invest in residential real estate4. They own lots of offices, and most malls you’ve ever been to. Something hasn’t made sense in the equation for them.

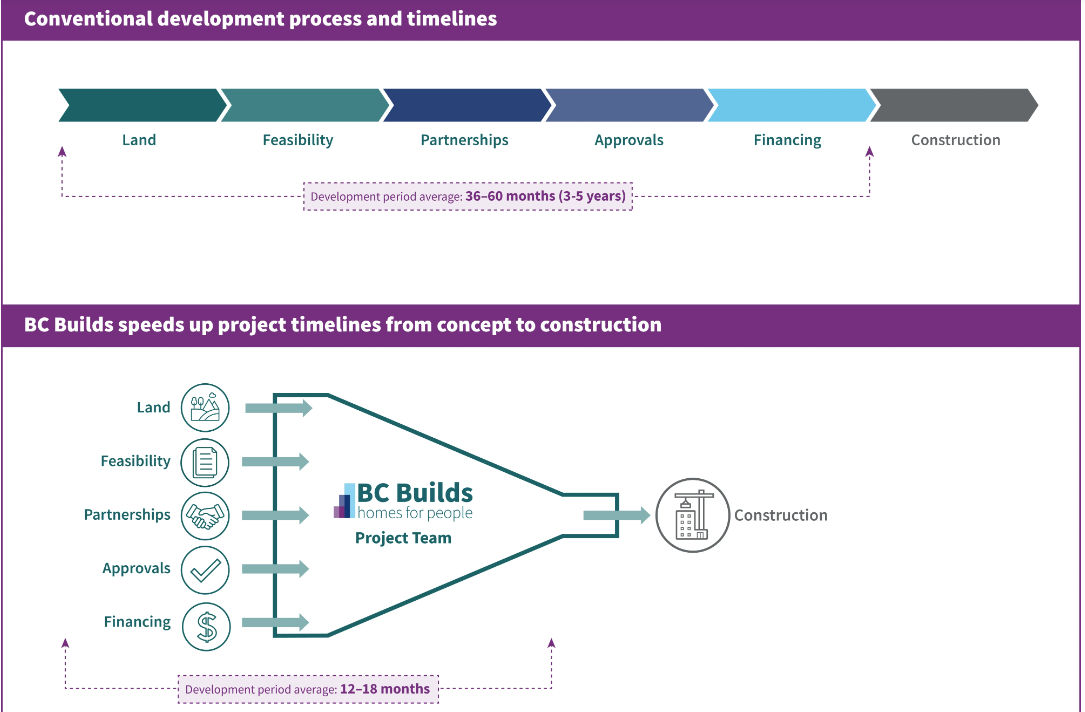

But I think pension funds could be a partner in programs like BC Builds (or its new federal cousin). BC Builds is an initiative to streamline and facilitate rental building activity. In exchange, rents need to be suitable for middle income households. Its not deeply affordable, but more targeted to the middle-class. The program also aims to use publicly-owned land where possible.

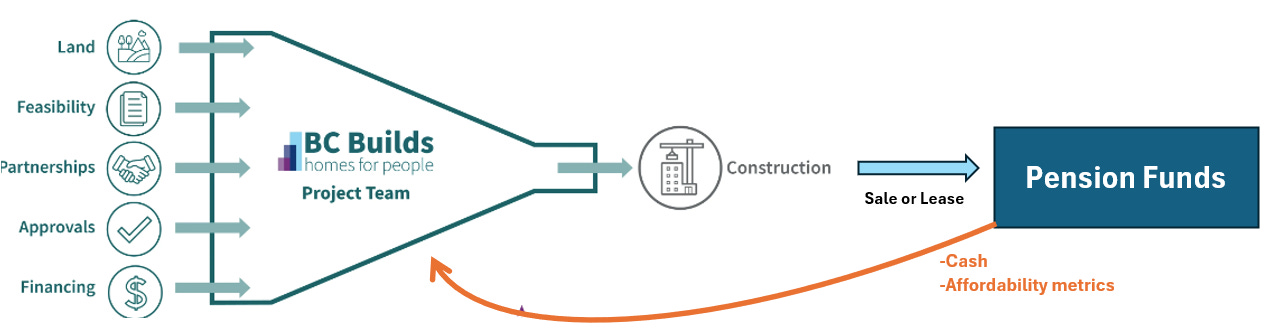

Pension funds likely don’t want to build anything (too risky), but they’d could be buyers once built. I can imagine a scenario where BC Builds identifies the land, gets approvals5, contracts out the construction, and then auctions the finished apartments to pension funds. In return, BC Builds would receive an upfront check (instead of waiting decades for the rent money).

Similarly, the federal Housing Plan has set an ambitious goal of building 250,000 units on public lands. The idea is for the homes to be built on land leased by the feds. That’s smart for feds, to keep ultimate control of the properties while monetizing it today. But most investors put a premium on owning/controlling their assets, and might be concerned about having a “hand-back” date, even if its decades away. Pension funds have experience with these lease structures (recall, infrastructure investments like the 407ETR toll road are generally leases/concessions).

Finally, affordability clauses, while generally bad for pure profit expectations, would likely make the future rental income more predictable (and that has some value to investors). If rents are set to 30% of incomes, well its much easier to predict income in 3 (or 30) years than it is to predict rents. With inflation protection you could create an interesting competitor to a typical bond.

The monetization of public lands would enable a “recycling” of capital into more construction financing or even land buying. Everyone involved, including and especially the construction companies, can specialize in what they do best.

In return, pension funds receive steady stream of rent, the kind of predictable cash flows that leads them to go buy infrastructure projects abroad.

Beyond price, there is also quantity. Canada needs to build 3.5 million homes to achieve affordability by 2030, and that’s on top of our current pace. Regardless of what you think of pension funds profit expectations, they one of the few real-world investors who can go from zero to billions of dollars invested quickly. They have the money, and the experience to pull it off. And they do it in far trickier markets than Canada, and far more complicated industries than housing.

Now, maybe it takes a sweetener. I think a special tax credit specifically for pension funds on future rental income would work. Some might say that’d be a waste of money, but we’ve made this deal recently for three EV battery plants, at a cost of $37bn. And unlike those foreign companies, this tax credit would cost Canadian taxpayers (all of us) in the future, to the benefit of Canadian pensioners (many of us), for housing that we get now. Sounds fine to me.

This is why pre-sale condos are so popular in Ontario. The pre-sale buyers give deposits that help fund construction, and get a (highly leveraged) investment in exchange. That worked, especially when Toronto condos were a sure-thing investment.

Imo, this is a big driver for the preference of condos, and especially, pre-construction condos, where builders get upfront deposits from future owners, and fully sells the units once the construction is finished.

And at least to start, maintenance and operations are modest costs compared to the upfront investment

CPP Investment has started to invest in residential real estate, and some others do, but it is still very small compared to other real estate types like office, commercial and industrial

Since this is the BC government, approvals here mostly means allowing themselves to build

Excellent explanation. In BC, QuadReal (the real-estate arm of the BCI pension fund for public-sector workers) is a major developer of rental housing.